Home Mortgage Financing

On Point Process made simple.

This might be the biggest decision of your life. Whether you are purchasing your new home or refinancing, we’ll take the stress out of financing and provide you with a smooth closing.

Your On Point Experience starts here.

Drop your info below and we’ll get in touch with you.

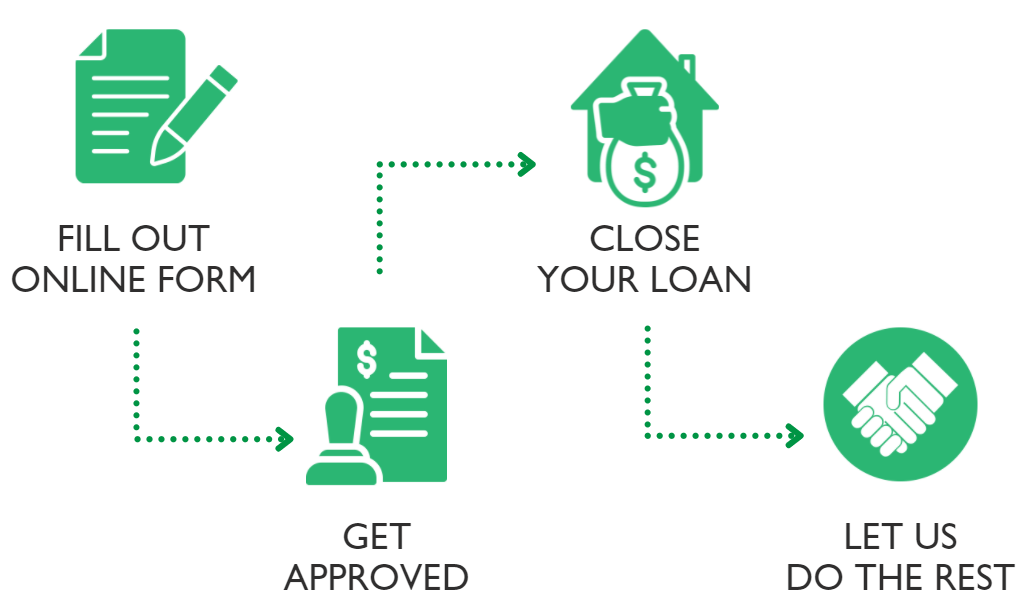

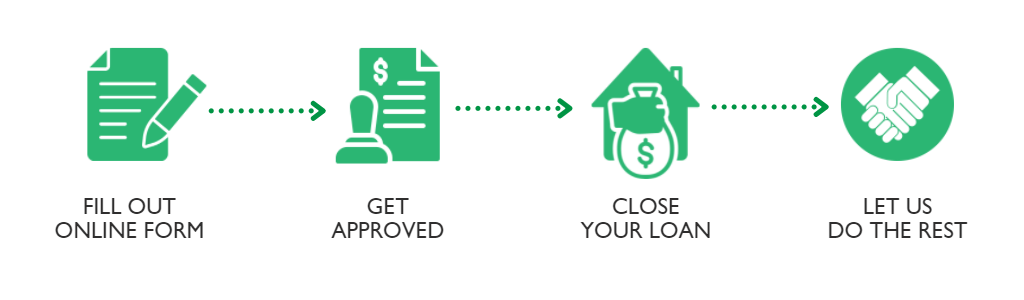

Online Form

Personalized Lending Experience

We provide a home mortgage that is tailored to your unique needs with the best loan and rate.

14-day Purchase Closing

We are committed to providing the fastest closing times in the industry so you can get the keys to your dream home as quick as possible.

5-STAR Loan Experience Rating

We take pride in providing the best client experience from start to finish.

Our clients are some of the happiest in the industry.

Here’s What they’re saying.

Frequently Asked Questions

On Point Home Loans, Inc. is an independent mortgage firm that is locally owned and operated in Charlotte, North Carolina. Our mission to empower each client to make the best decisions for their individual financial futures.

After years of working for large banks and retail lenders, the founders of On Point saw a considerable amount of time and money was invested in expensive advertising and elaborate corporate structures, which often resulted in loans that were highly overpriced. This inspired them to take a more personal approach to lending that made their clients’ financial needs a priority.

As an independent mortgage broker, the team at On Point Home Loans are able to focus on the customers’ best interests by delivering a wider variety of mortgage products at more affordable terms.

FHA

An FHA loan is a mortgage loan that is insured by the Federal Housing Administration (FHA). Essentially, the federal government insures loans for FHA-approved lenders in order to reduce their risk of loss if a borrower defaults on their mortgage payments.

The FHA program was created in response to the rash of foreclosures and defaults that happened in 1930s; to provide mortgage lenders with adequate insurance; and to help stimulate the housing market by making loans accessible and affordable.

VA home loans

A VA loan is a mortgage loan in the United States guaranteed by the U.S. Department of Veterans Affairs (VA). The loan may be issued by qualified lenders. The VA loan was designed to offer long-term financing to eligible American veterans or their surviving spouses (provided they do not remarry).

The FHA program was created in response to the rash of foreclosures and defaults that happened in 1930s; to provide mortgage lenders with adequate insurance; and to help stimulate the housing market by making loans accessible and affordable.

Non-QM loans

30-year fixed-rate loans

Adjustable-rate mortgage options

USDA home loans

Jumbo home loans

A jumbo loan is a loan that exceeds the conforming loan limits as set by Fannie Mae and Freddie Mac. As of 2019, the limit is $484,350 for most of the US, apart from Alaska, Hawaii, Guam, and the U.S. Virgin Islands, where the limit is $726,525. Rates may be a bit higher on jumbo loans because lenders generally have a higher risk.

Hard money loans

Construction to permanent loan

Affordability – Interest only payments during construction

Quick draw turn times

The annual percentage rate (APR) is an interest rate reflecting the cost of a mortgage as a yearly rate. This rate is likely to be higher than the stated note rate or advertised rate on the mortgage, because it takes into account points and other credit costs. The APR allows homebuyers to compare different types of mortgages based on the annual cost for each loan. The APR is designed to measure the “true cost of a loan.” It creates a level playing field for lenders. It prevents lenders from advertising a low rate and hiding fees.

The APR does not affect your monthly payments. Your monthly payments are strictly a function of the interest rate and the length of the loan.

Because APR calculations are effected by the various different fees charged by lenders, a loan with a lower APR is not necessarily a better rate. The best way to compare loans is to ask lenders to provide you with a good-faith estimate of their costs on the same type of program (e.g. 30-year fixed) at the same interest rate. You can then delete the fees that are independent of the loan such as homeowners insurance, title fees, escrow fees, attorney fees, etc. Now add up all the loan fees. The lender that has lower loan fees has a cheaper loan than the lender with higher loan fees.

The following fees are generally included in the APR:

- Points – both discount points and origination points

- Pre-paid interest. The interest paid from the date the loan closes to the end of the month.

- Loan-processing fee

- Underwriting fee

- Document-preparation fee

- Private mortgage-insurance

- Escrow fee

The following fees are normally not included in the APR:

- Title or abstract fee

- Borrower Attorney fee

- Home-inspection fees

- Recording fee

- Transfer taxes

- Credit report

- Appraisal fee

Below is a list of documents that are required when you apply for a mortgage. However, every situation is unique and you may be required to provide additional documentation. So, if you are asked for more information, be cooperative and provide the information requested as soon as possible. It will help speed up the application process.

Your Property

- Copy of signed sales contract including all riders

- Verification of the deposit you placed on the home

- Names, addresses and telephone numbers of all realtors, builders, insurance agents and attorneys involved

- Copy of Listing Sheet and legal description if available (if the property is a condominium please provide condominium declaration, by-laws and most recent budget)

Your Income

- Copies of your pay-stubs for the most recent 30-day period and year-to-date

- Copies of your W-2 forms for the past two years

- Names and addresses of all employers for the last two years

- Letter explaining any gaps in employment in the past 2 years

- Work visa or green card (copy front & back)

If self-employed or receive commission or bonus, interest/dividends, or rental income:

- Provide full tax returns for the last two years PLUS year-to-date Profit and Loss statement (please provide complete tax return including attached schedules and statements. If you have filed an extension, please supply a copy of the extension.)

- K-1’s for all partnerships and S-Corporations for the last two years (please double-check your return. Most K-1’s are not attached to the 1040.)

- Completed and signed Federal Partnership (1065) and/or Corporate Income Tax Returns (1120) including all schedules, statements and addenda for the last two years. (Required only if your ownership position is 25% or greater.)

If you will use Alimony or Child Support to qualify:

- Provide divorce decree/court order stating amount, as well as, proof of receipt of funds for last year

If you receive Social Security income, Disability or VA benefits:

- Provide award letter from agency or organization

Source of Funds and Down Payment

- Sale of your existing home – provide a copy of the signed sales contract on your current residence and statement or listing agreement if unsold (at closing, you must also provide a settlement/Closing Statement)

- Savings, checking or money market funds – provide copies of bank statements for the last 3 months

- Stocks and bonds – provide copies of your statement from your broker or copies of certificates

- Gifts – If part of your cash to close, provide Gift Affidavit and proof of receipt of funds

- Based on information appearing on your application and/or your credit report, you may be required to submit additional documentation

Debt or Obligations

- Prepare a list of all names, addresses, account numbers, balances, and monthly payments for all current debts with copies of the last three monthly statements

- Include all names, addresses, account numbers, balances, and monthly payments for mortgage holders and/or landlords for the last two years

- If you are paying alimony or child support, include marital settlement/court order stating the terms of the obligation

- Check to cover Application Fee(s)

Simply fill out the online form and one of our loan advisors will contact you.

You can also call us at 833-955-6267 or email us at info@ophomeloans.com.

Or, visit our office at 1200 The Plaza Unit G2 Charlotte, NC 28205. Our office hours are Monday – Friday 8:00 – 8:00 PM, Saturday 9 AM – 7 PM.

Connect with our expert loan advisors